I’ve always loved learning how things work. So when we bought our first home, I was both frustrated at how hard the mortgage industry works to confuse buyers and determined to figure the system out. I learned a lot when we signed that first mortgage, and even more when I did three no-cost refinances on our first home.

When we moved on to our second home, I came up with an idea to combine the best hacks for purchasing and refinancing into the crazy scheme that follows — how to get your lender to pay you (not only closing costs, but prepaid interest, escrows, and many other fees you can bundle in) to buy your house.

This may not work for everyone, but if you can meet the prerequisites, are willing to accept the risks, and can find a lender that will give you this kind of loan, you can save thousands of dollars when you buy your next home.

Prerequisites

20% down payment. For this process to work, it’s best to have at least a 20% down payment. Why? In order to refinance in step 4 with the lowest possible rate, you’ll likely need to put 20% down. All of the refinances I’ve done have required at least 20% equity. It may be possible to follow this process with less than 20% down, but I haven’t done it and I wouldn’t recommend it.

High credit score. The lender I used required a combined credit score (average of all three credit bureaus) > 740 to get the best rate and not pay any additional fees on the mortgage. Since you’ll be getting two lenders to do hard credit pulls, make sure your score is above the score needed for both lenders to get the best rate BEFORE you start this process.

Two lenders. My initial lender had a rule that they would not accept refinances for mortgages they originated for six months. Because I was going to be getting an above-market interest rate, I wanted to refinance before six months to lower my rate, so before starting this process I found a second lender who would let me refinance as soon as I purchased the house.

Risks

Interest rate risk. If you do steps 1-3, and then interest rates dramatically rise before you can refinance, you may be stuck with an interest rate higher than what you want. I think this is a pretty low risk.

Failure to refinance risk. Another risk is that for some reason you won’t be able to refinance – maybe you lose your job, or your financial situation changes some other way that makes you a less attractive borrower. Keep these risks in mind – if you are concerned about them, it may not be worth it to save a few thousand dollars up front only to pay multiples of that over the life of your mortgage.

While these risks are worth considering, I still highly recommend this process for people who meet the prerequisites. I find both bad scenarios far less likely than what usually happens – interest rates do not move quickly, and people generally stay employed. Also, most people do not live in their house for the life of their mortgage anyways.

With those out of the way, let’s get into the details of the process.

Step 1: Find a lender that will sell you an above-market rate for negative points

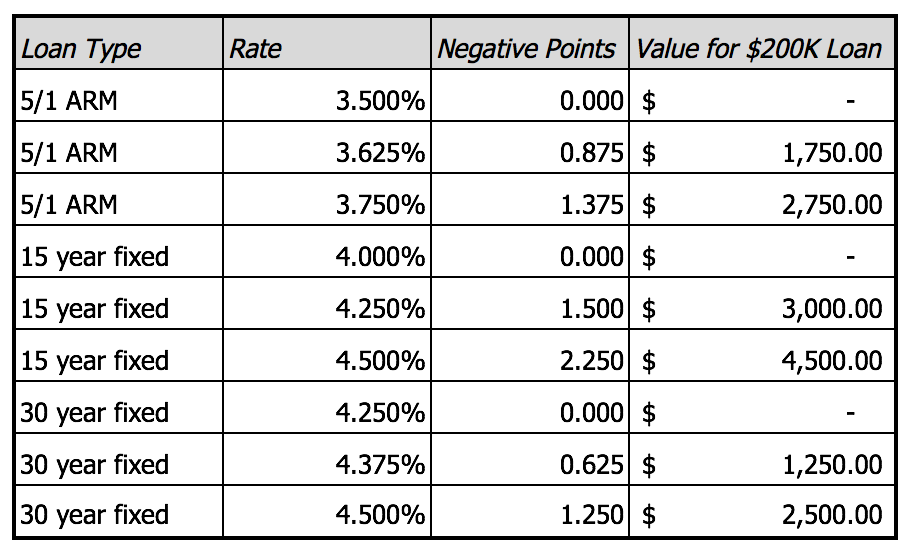

The first step is the “secret sauce” of this process. While many lenders advertise rates on their websites, they don’t usually advertise “above market” rates. These are simply higher interest rates that the lenders will offer for a credit. For example, instead of a 3.5% rate, the lender would give you a 3.75% rate with a credit of 0.5 “points.” What are points? They are just percentages of the loan amount. So for a $200,000 loan, one point is $2,000. (The mortgage industry and financial services industry in general loves to make simple things complicated by introducing confusing terminology).

So you need to find a lender who will do this. Many lenders may offer this even if it’s not advertised on their site. The lender I used is a local lender in Virginia and North Carolina called CapCenter. They offer negative points, but you have to call them to get the negative point options. To further complicate things, rates change daily, and the negative point options change daily with them. They are also different based on the loan type (length of term, fixed vs. variable). Since you will be refinancing immediately after closing, the loan type doesn’t matter. To do step #2 correctly, you’ll need to build a table of all of the options for all loan types. Here’s an example of what that may look like.

Step 2: Line up your settlement costs to match the negative points

A key thing to remember is that the negative points can ONLY be used to offset settlement costs on the mortgage. You can’t get a 82% mortgage with $50K in lender refunds and use that money toward your down payment. My lender actually wouldn’t let me get a loan that had negative points greater than my settlement costs. Your mileage may vary – but you don’t want to get a loan like this because anything that goes above your settlement costs will be wasted.

So how do you match settlement costs to the points? This part can be a bit tricky. First, you’ll need your lender to give you a loan estimate. This is a document that lenders have to provide using a standard form mandated by the Consumer Financial Protection Bureau (see a good example with explanations of the form on the CFPB website here).

When you get the loan estimate, you’ll need to look at a few things:

On page 1, make sure that Prepayment Penalty says NO like it does in the example below from my mortgage.

On page 2, Section J entitled Total Closing Costs shows your total costs (labeled D+I) and your lender credit. Your total closing costs are D+I minus your lender credit. The D+I number is your total settlement costs. If this loan estimate already had the negative points, then you can see what the lender credit is. The goal is to get the lender credit as close to matching the D+I number without going over it.

The example below is my mortgage. You can see the closest I could get was to be ~$184 off from my settlement costs.

So where is the free money? From the example I shared, it still looks like I paid $184 for my loan. While technically that is true, you have to look at what the negative points covered. On page 2 of the loan estimate, A, B, C and D are all costs of getting a loan (which is why they are helpfully called Loan Costs). On the contrary, E, F, G and H are mostly expenses that everyone has to pay when buying a house. Even if I bought a house with cash, I would have to pay:

- Recording fees / transfer taxes (E)

- Insurance premiums (part of F and G)

- Property taxes (G)

- Inspection and title insurance (I)

In my example, these fees associated with buying a home added up to $4,650. Again, even if I paid cash for my house, I would still pay this $4,650. So while I technically did pay $184 in “closing costs”, in reality, the lender actually paid me $4,650 for a 4.125% loan with negative points instead of a 3.875% loan with zero points.

Now the only additional cost to factor in is the difference between my interest payments between my negative point loan and the zero point loan. In my case, that difference worked out to be ~$200/month, meaning that my negative point rate was going to cost me $200/month more in interest. As long as I could refinance to a better loan in ~23 months, I would be making more money with this set up than with just going with the zero point loan to start.

Step 3: Close on your “free” mortgage

Once you’ve found the right mortgage product that gives you the closest negative points to match your settlement costs, the next step is to close on the loan. This works the same as any other mortgage closing & home buying process, except you don’t need as much money for your down payment because the lender is paying for all your loan fees + the other costs associated with buying a home even without a loan.

Step 4: Refinance!

Now that you’ve closed on your loan and reaped the thousands of dollars in benefits from your lender, you can immediately begin the process of refinancing. In my case, as I mentioned above, I had already selected my second lender to use for the refinance, Third Federal. As soon as I closed on my loan, moved into my house, and received the paperwork from my lender (~1 month after closing) I put in my application to refinance with Third Federal.

While Third Federal provided a great loan, they did take a loooong time to complete the refinance. I ended up holding my 4.125% loan for ~6 months, which knocked about $1,200 off my initial $4,650 in savings. This left me with a net payout of $3,450 from my first lender (thanks Chase!).

So there you have it – using this strategy you should be able to get your lender to pay your transfer taxes, homeowners insurance, and a bunch of other fees that you’ll incur when buying a house. Note that this strategy works even better if you can pay cash for a house – simply complete steps 1-3, then instead of refinancing in step 4, immediately pay off the loan. If I had the cash to buy my house outright, I could have saved nearly the full $4,650. It’s definitely bizarre to think that you can make money by financing a house even if you have cash and then immediately pay it off, but it actually works out that way.

Happy mortgage hacking!

This is so interesting!! I am going to share this with the hubs…he also likes learning about mortgages! 🙂

I’ll be right back. I’m gonna go take a “Mortgage Verbiage 101”. I love the thought of doing this! Pinned it! I’m gonna go do some homework and then come back and decipher what all of this means.

Thank you for all of this valuable information!

hahah! i’m glad you liked it!

So much of the information provided in this post is inaccurate. And, why would you advise someone to take a risk like that? Especially in a rising rate environment.

Thanks for the comment! Can you share what you see as inaccuracies? You are correct that this approach may not be the best choice in a rising rate environment. Even in today’s environment, rates are not rising that quickly. But this approach is not for everyone – sounds like it’s not for you.

What were your costs to refinance?

Hi Kendra – I recommend lining up a second lender who offers a no cost refinance. In the case of this loan, I refinanced into a loan with Third Federal – no closing costs other than a $295 fee.

Unfortunately this isn’t all accurate. First your lender didn’t want to refinance you until after 6 months because we get penalized substantially when clients pay off early (before 6 payments are made) it’s called an EPO early pay off. A $400k loan could be as much as $20k penalty to the lender office. We can’t stay in business by doing that. So we ask clients to just wait until the 6 mos mark. Second, the negative points you mentioned is called a Lender Credit. It’s from the above par pricing you chose (any reputable lender will give you this option) and you can choose a higher rate to cover closing costs and prepaids. Btw this is for a refinance or a purchase. However, most people won’t choose to do this generally because it’s not a free loan .. you just hiked up your payment from the higher rate. However it’s worth exploring the option. I am a mortgage lender of 27 years who believes in educating my clients thoroughly on buying and refinancing. Just wanted to clarify a few things in your blog post @LetsTalkMortgagePro

Hi – thanks for stopping by LetsTalkMortagePro.

Responding to your first point, it is immaterial to me what the lender wanted or did not want me to do (and this is not an inaccuracy). The lender allowed me to take out a loan with a higher rate and larger lender credit and then pay it off. If the lender didn’t want me to pay off the loan immediately, they should not have allowed it. Also, it ended up taking about six months anyways.

Second, yes that is what I explained in the post. Which part of my explanation was inaccurate? I explain that the higher rate is the price you pay for the higher lender credit, and that you have to factor that in for as many months as you carry the loan before refinancing. But remember, I refinanced in ~6 months. So instead of saving $4,650, I saved $3,450 because of the six months of interest payments at the higher rate. Most people won’t want to get one loan then immediately refinance, and that’s fine. But for those who are willing to do the work, it can be quite lucrative.

Thanks, Tom